In an ever-evolving economic landscape, small businesses often find themselves in need of financial support to kickstart or expand their operations. The Prime Minister's Employment Generation Programme (PMEGP) is a government initiative designed to provide loans to small entrepreneurs, particularly in rural and semi-urban areas. Understanding the PMEGP loan rules is crucial for potential applicants to navigate the application process smoothly and ensure that they meet the necessary criteria.

The PMEGP loan rules encompass various aspects, including eligibility criteria, documentation requirements, loan amounts, and repayment options. By familiarizing yourself with these rules, you can better prepare your application and increase your chances of securing the funding you need. This article aims to provide a comprehensive overview of the PMEGP loan rules, helping aspiring entrepreneurs understand what is required to access this vital financial resource.

As the government continues to emphasize entrepreneurship as a means of job creation, understanding the PMEGP loan rules will empower individuals to take control of their financial future. Whether you are a first-time entrepreneur or looking to expand an existing business, this guide will equip you with the knowledge necessary to make informed decisions regarding your loan application.

What is the PMEGP Loan?

The PMEGP loan is a financial instrument provided by the Government of India to promote self-employment and entrepreneurship among the youth. This scheme is implemented by the Ministry of MSME (Micro, Small, and Medium Enterprises) and aims to provide financial assistance through banks, making it easier for individuals to start their own businesses.

Who is Eligible for PMEGP Loans?

Eligibility criteria are crucial in determining who can apply for PMEGP loans. Here are the primary eligibility requirements:

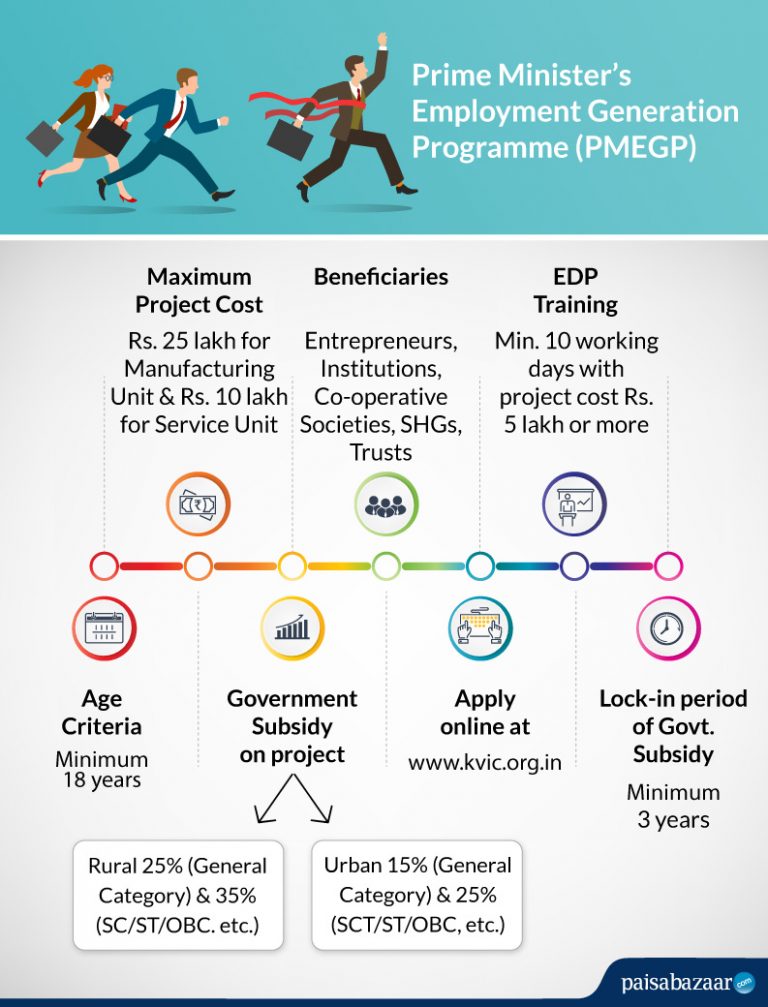

- Applicants must be at least 18 years old.

- Both new and existing businesses can apply, but existing businesses must not have been operational for more than 3 years.

- Individuals must be Indian citizens.

- Specific educational qualifications may be required based on the nature of the business.

- Self-help groups (SHGs) and cooperatives can also apply.

What Are the Types of Businesses That Can Apply?

The PMEGP loan can be availed for various types of businesses, including:

- Manufacturing units

- Service sectors

- Retail businesses

- Agro-based industries

- Handicrafts and handlooms

What Are the Loan Amounts Available Under PMEGP?

The PMEGP loan scheme provides a significant amount of financial assistance to eligible applicants. The loan amounts vary based on the type of business and the project cost:

- For manufacturing units, the maximum loan amount can go up to ₹25 lakh.

- For service and business sectors, the maximum loan amount can be ₹10 lakh.

What Are the Interest Rates and Repayment Terms for PMEGP Loans?

The interest rates for PMEGP loans are competitive and designed to be affordable for small entrepreneurs. Typically, the interest rate is around 10% to 12%, depending on the lending bank. The repayment period is generally set between 3 to 7 years, which allows borrowers to manage their finances effectively.

What Documents Are Required for PMEGP Loan Application?

To apply for a PMEGP loan, applicants need to submit various documents, including:

- Identity proof (Aadhar card, PAN card, etc.)

- Address proof

- Project report detailing the business plan

- Educational qualifications

- Bank account statement

How to Apply for PMEGP Loans?

Applying for a PMEGP loan involves a systematic approach. Here’s a step-by-step guide:

- Prepare a detailed project report.

- Gather all necessary documents.

- Visit the nearest bank or financial institution offering PMEGP loans.

- Submit your application along with the required documents.

- Await approval and prepare for loan disbursement.

What Are the Key PMEGP Loan Rules to Remember?

Understanding the PMEGP loan rules is essential for a smooth application process. Here are some key rules to keep in mind:

- The loan is provided on a subsidy basis, which means that a portion of the loan may be subsidized by the government.

- Timely repayment is crucial, as defaulting can affect future borrowing opportunities.

- Ensure that the project aligns with the objectives of the PMEGP scheme.

What Are the Benefits of PMEGP Loans?

The PMEGP loan scheme offers several advantages for small entrepreneurs:

- Financial assistance for starting or expanding a business.

- Subsidized interest rates make loans more affordable.

- Encourages self-employment and job creation in local communities.

In conclusion, the PMEGP loan rules provide a vital framework for aspiring entrepreneurs to access financial support for their business ventures. By understanding the eligibility criteria, loan amounts, interest rates, and application process, potential borrowers can effectively navigate the opportunities provided by this scheme. Whether you are looking to launch a new business or grow an existing one, the PMEGP loan can be an essential tool in your entrepreneurial journey.

The Future Of Education: ST Scholarship 2024

Understanding HDFC Personal Loan EMI Payment: A Complete Guide

Discovering 9xmovie.diy: Your Ultimate Movie Streaming Destination